Can You Actually Save Money by Buying When Rates Are Higher?

Photo by Sasun Bughdaryan on Unsplash

Mortgage rates have been much in the news over the past several months, with rates having raised considerably since their historic lows in 2021. News of increased interest rates tends to spook prospective buyers, who perceive the higher rates as a detriment to their buying power. However, while it may seem counterintuitive, buying a home when mortgage rates are higher can actually be a smart financial move in the long run. Here we will explore several compelling reasons why buying a home when interest rates are higher can save you money and set you up for potential financial gains.

Reduced Buyer Competition

Higher mortgage rates often deter potential buyers from entering the housing market. This reduction in buyer competition can work to your advantage. With fewer buyers vying for the same properties, you may encounter less competition during the negotiation process. Moreover, sellers may be more willing to make concessions such as credits. This can increase your chances of landing the property you want at the price that works for you.

Downward Pressure on Prices

Higher mortgage interest rates typically put downward pressure on home prices. As rates increase, the affordability of homes decreases, leading to decreased demand in the housing market, resulting in more attractive prices. Conversely, when rates go back down, prices will tend to climb again, so waiting for rates to drop could work against you.

Hypothetically, let’s say you buy a property today with a 20% deposit and a mortgage rate of 7%. Here are two price points for reference. (Note that rates are constantly shifting. We are happy to run scenarios based on current rates.)

| Home price | Deposit | Loan | Mortgage Rate | Principal & Interest (Monthly) |

|---|---|---|---|---|

| $1,100,000 | $220,000 | $880,000 | 7% | $5,855 |

| $800,000 | $160,000 | $640,000 | 7% | $4,258 |

Now let’s say you held out until rates dropped to 6%. The catch is that the price on those same properties has increased by $100,000 due to increased buyer demand.

| Home price | Deposit | Loan | Mortgage Rate | Principal & Interest (Monthly) |

|---|---|---|---|---|

| $1,200,000 | $240,000 | $960,000 | 6% | $5,756 |

| $900,000 | $180,000 | $720,000 | 6% | $4,317 |

As you can see, even though the interest rate is lower, with the increased price on the property, the monthlies are roughly equivalent — and you’ve had to put down more for the deposit. That’s money you could have invested elsewhere, further increasing your gains.

Refinancing Opportunities

Higher interest rates are not permanent. Over time, rates tend to fluctuate, and there may come a time when they decrease again. If you initially bought a home when rates were higher, you can take advantage of future rate reductions by refinancing your mortgage. Refinancing allows you to secure a lower interest rate, reducing your monthly mortgage payments and potentially saving you a significant amount of money over the life of the loan. Let’s take a look at what would happen if you purchased those above properties today at 7%, and then refinanced when rates dropped to 6% — even if you paid nothing against the principal in the interim.

| Home price | Deposit | Loan | Refi Mortgage Rate | Principal & Interest (Monthly) |

Monthly Savings |

|---|---|---|---|---|---|

| $1,100,000 | $220,000 | $880,000 | 6% | $5,276 | $579 |

| $800,000 | $160,000 | $640,000 | 6% | $3,837 | $421 |

Think of it this way: If you bought at the higher rate and refinanced when the rates dropped, you would be paying hundreds of dollars less per month than if you waited to buy at the lower rate. Plus, you put down less money up front, keeping money in your pocket.

Lower Property Taxes

Property taxes are based on the purchase price, and grow incrementally based on annual adjustments for inflation, not to exceed 2%. Property taxes in California are 1% of purchase price, plus any city and local supplements. For example, the yearly property tax rate in San Francisco for 2022/2023 was 1.1797%. The lower your purchase price, the less you pay out in taxes each year over the entire time you own the property.

Mortgage Interest Deductions

One of the benefits of home ownership is the ability to deduct mortgage interest from your taxable income (up to a loan amount of $750,000). Higher mortgage rates result in larger interest payments, which translates into greater tax deductions. Always consult your tax professional for the most accurate information.

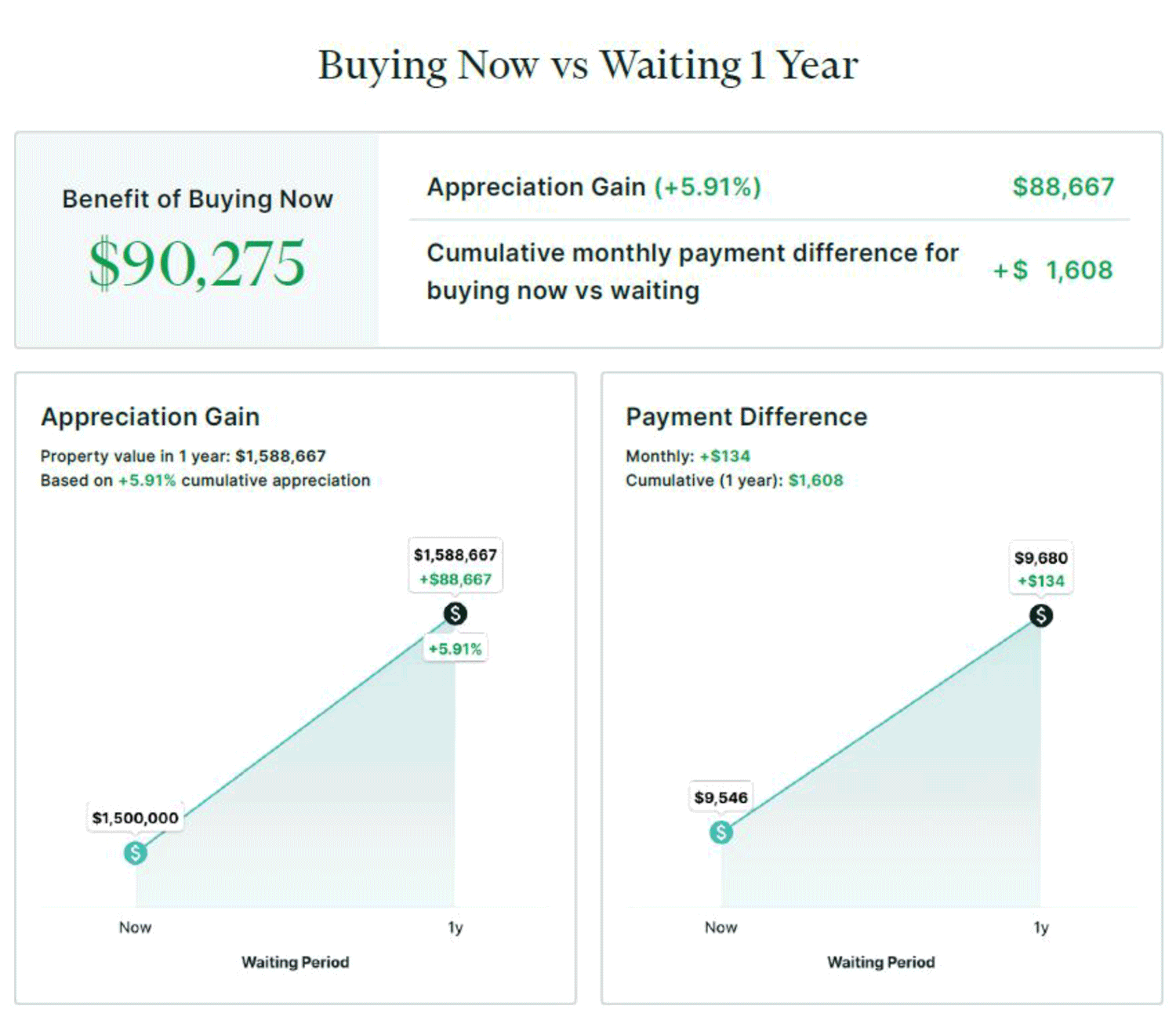

Potential for Greater Upside

This is simple economics: Buy low, sell high. Buying a home at a lower price during a period of higher interest rates can position you for potential future gains as property values rise. As the housing market stabilizes and interest rates eventually decrease, the value of your property could appreciate significantly, possibly more than if you had purchased at a higher price, resulting in potential equity gains.

In this example provided by Risha Kilaru of OriginPoint, Compass’s preferred lender, waiting to purchase for one year could cost you potential appreciation of more than $88,000. Moreover, given that price differential, if you buy a year later, your monthly mortgage payments will be higher as well.

So you see, there are many levers to consider when financing a home. Mortgage rate is an important factor, but there are others that impact the long-term benefits of home ownership.

Ready to jump in the market? Let us connect you with our amazing financing team, who will set you up for success.